Skip to content

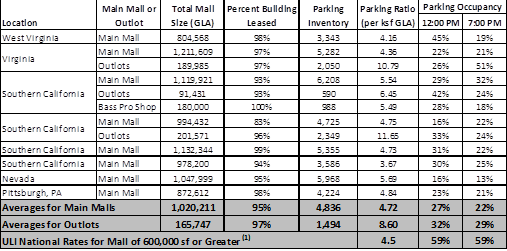

Skip to content I previously conducted a parking study of eight malls across America. This included malls in Southern California, West Virginia, Virginia, Nevada, and Pennsylvania. Some of these malls had outlots, which are essentially strip malls separated from the mall by access roads. These outlots were included in the analysis, but they included their own parking lots. We analyzed the parking inventory and parking occupancy during a typical weekday in February during the hours of 12 PM and 7 PM. Based on the parking occupancy counts and square footages of the malls, we calibrated the parking demand ratios in Urban Land Institutes (ULI) shared parking model. We also calculated the simple parking ratio per 1,000 s.f. of gross leasable area at each mall. The data collected is summarized in the table below.

Parking Occupancy versus Retail Occupancy

As shown, these are large malls that have approximately 1 million square feet of gross leasable area. The eight malls had an average leasable area occupancy of 95%, which shows they are fairly successful malls. However, the parking demand at these malls is sufficiently low with an average occupancy of 27% during the 12 PM period and 22% during the 7 PM period. This is well below the projected parking occupancy during the month of February during these time periods, which should be around 60% occupancy, based on the ULI shared parking model. It’s not as if these were dilapidated malls with outdated stores. They each had popular anchor stores (i.e. Macy’s, Nordstrom, Sears, etc.) and your basic cast of complimentary stores (i.e. Banana Republic, Urban Outfitters, J Crew, etc.). They each had a food court and some restaurants.

Is ULI Occupancy Data Outdated?

So what does this data mean exactly? Well I think that it says that malls are not as popular as they once were and that the parking data provided in the ULI shared parking model regarding shopping centers is somewhat outdated. This ULI data is suppose to be based on parking occupancy counts of malls similar to the ones provided in the table below, but the data shows a huge discrepancy compared to the ULI data. However, the parking ratio of the inventory of spaces provided per 1,000 s.f. of GLA is fairly consistent, 4.5 for ULI and 4.72 for the eight malls analyzed. This is primarily because the number of spaces provided at malls is based on zoning code standards for the region, which may defer to the information provided in ULI’s Shared Parking or the Institute of Transportation Engineers Parking Generation.

Is Christmas to Blame for Overdesigned Parking?

Even though there was such a low occupancy in February at these malls (27% at 12 PM and 22% at 7 PM), I bet that if I performed counts during the month of December (holiday season) each of the mall’s parking lots would be full. So essentially, we have Christmas to blame for our overdesigned mall parking facilities. This is nothing to quiver at, considering the amount of paved land area that sits unused for more than 90% of the year collecting storm water and preventing further development or green space in the area. Based on the analysis, a mall with no garages and only surface lots would have approximately 1,059,000 s.f. of paved parking lot area which would sit unused for approximately 90% of the year. So what is the reason that malls are becoming less popular?

Mall and Outlots Parking Study Data

Quick History of Malls

The popularity of traditional malls came along with the explosion of the suburbs during the fifties. Fully enclosed shopping malls, as we know them today, with parking, anchor stores and restaurants first started being developed in the mid 1950’s. It was the convenience that attracted people: free parking, an enclosed air-conditioned environment, and a plethora of stores to choose from. They stole shoppers from independent stores located on Main Streets throughout America. They also attracted the power walkers and loitering teenagers. Admit it, if you grew up in the suburbs you spent a many of nights during your teen years walking the halls of a mall trying to act cool. Malls became the public centers in many suburbs or cities that lacked a vibrant downtown or a really nice Wal-Mart. In the mid 1990’s malls were being constructed at a rate of 140 malls per year. However, by the twenty-first century the construction of malls had declined, and in 2007, a year before the stock market crash, no new malls were constructed in America. That had not happened in America for 50 years. The first new mall to be opened in America since 2007 was in March 2012 in Salt Lake City. There is even a website dedicated to the death of malls (http://deadmalls.com/).

Conversion to Lifestyle Centers

I believe the unpopularity and death of malls is due to a number of things. I think people are obviously doing more online shopping and shopping at big box outlets usually located in strip malls, which are more convenient options over a visit to the mall. However, I also think people would rather visit a true city center if they are going to spend a good part of their day shopping. They are getting sick of the stale and uncultured mall environment. Developers and investors have recognized that this is the trend, and they became creative in keeping these REIT driven money generating malls alive. So they ditched the traditional indoor mall layout and began developing lifestyle centers. A lifestyle center has a more outdoor city center concept, which includes a mix of other land uses, such as: residential, office, and event centers. They are designed to replicate a beautiful city center with through streets and pedestrian amenities (i.e. benches, fancy lighting, brick walkways, on-street parking and street art). An example of a lifestyle center is The Glen in Glenview, Illinois. With the addition of other land uses (i.e. office, residential, recreation) there are now more opportunities for shared parking, which can help reduce the amount of parking spaces unused for a good part of the year. However, I personally think that these lifestyle centers will have a short shelf life and people will soon see through the same cookie-cutter stores and regurgitated mall feel. People want true vibrant city centers that offer an independent, eclectic and original environment.